An in-depth analysis of the European regional airline market and its development within the last five years, 33% of all regional carriers in Europe went out of business between 2008 and today, nearly one fourth of the employees lost their jobs. …

__________________________________________________________________________________________

Authors: Hanna Schaal (PROLOGIS) schaal@prologis.aero and Max Oldorf (ch-aviation) max.oldorf@ch-aviation.ch

__________________________________________________________________________________________

Are European Regionals’ Successful Days Numbered?

To download the following analysis as a PDF file click here.

33.33% of all regional carriers in Europe went out of business between 2008 and today, nearly one fourth of the employees lost their jobs. PROLOGIS and ch-aviation have scrutinized Europe’s regional airline market.

Doesn’t it sometimes feel like Europe’s regional airlines’ market exits are as common as their entries? Don’t you occasionally wonder if this industry still bears any potential? In order to gain clarity in this matter, PROLOGIS and ch-aviation conducted a study of the European regional market, comparing data from 2008 with data from 2013.

The results are quite frightening: 44 new airlines were founded from 2008 on, 22 of them have already vanished. The overall mortality rate was 33.33%.

But the most concerning number is probably a job loss rate of 23 % between 2008 and today, which means that almost every fourth employee lost his job.

It seems like regional carriers’ successful days are history.

The Affiliates – Dwindling Partnerships

It all started in the early days with the traditional regional carrier model, which is still very popular today. Affiliated airlines supply or ‘feed’ large network carriers’ hubs with passengers from small, nearby regional airports. In many cases, the relationship between network airlines and the subcontractors is based on a parent-subsidiary model, with the affiliates operating either under their own brands or a regional brand. Lufthansa, for example, currently has four regional partners (Air Dolomiti, CityLine, Eurowings and Augsburg Airways), all 100% subsidiaries with the exception of Augsburg Airways that together form Lufthansa Regional. Nevertheless, the Augsburg Airways regional partnership will be terminated at the end of Lufthansa’s summer schedule 2013 after 16 years due to the German legacy carrier’s restructuring program ‘Score’.[1] Along with the previous termination of the equally longstanding partnership with Contact Air in October 2012, the German airline will have parted from two regional partners within only a year.

A similar decrease in regional affiliated partnerships can be observed at Air France-KLM and IAG (International Airlines Group, holding company of British Airways & Iberia). To cut costs, Air France will be merging the three regionals Airlinair, Brit Air and Régional under a single new brand called ‘Hop!’ as of March 31, 2013, that will operate most non-hub routes with a low-cost carrier like product offering.[2] British Airways already sold its regional BA Connect to British regional Flybe. in March 2007, as the management did “not see any prospect of profitability in its current form”[3] anymore.

All three major European carrier groups not only face increasing pressure from still fast growing low-cost carriers for traffic within Europe. They also feel competition from expanding international carriers, increasingly serving smaller European markets, from hubs in the Middle East for example. These factors have led to lower yields for point-to-point regional traffic and lower demand for hub and spoke traffic within Europe as well as for intercontinental flights. This makes it difficult to continue profitable regional operations with small aircraft.

The Independents – Decreasing Profits?

Flybe. – the keyword that reminds us that when we talk about regional carriers, we are not only referring to affiliates. Since the mid-1990s, there have been a growing number of totally independent carriers that offer point-to-point service to both small regional and large international airports, operating under their own brands and with no ties to large network carriers. Since the acquisition of BA Connect in 2007 we just mentioned, Flybe. is Europe’s largest regional carrier in general. For the six months until 30 September 2012, however, the group that includes Flybe. Nordic (a joint venture with Finnair) reported a pre-tax loss of £1.3m (€1.5m). Flybe. blamed the results on fuel prices at record highs and a decrease in passenger numbers in the UK domestic aviation market.[4] The Norwegian regional Widerøe, that is still fully owned by SAS (with a sale expected this year [5]), but operating fairly independently, was selected European Airline of the Year 2012 by the ERA (European Regional Airline Association). Yet, the award cannot hide the fact that the carrier’s operating profit decreased by 59.8% between December 2011 and October 2012. Other European independents must deal with financial results similar to Flybe.’s and Widerøe’s.

Regionals in Europe: Overall Analysis Results

How did we obtain our results and what do they look like in greater detail? In order to analyze Europe’s regional carrier market and its development within the last five years, we compared airline and fleet data from January 1, 2008, with current data (date of data analysis: February 17, 2013). Regionally, the scope of the study includes all EU member states plus Albania, Bosnia-Herzegovina, Croatia, the Faroe Islands, Iceland, Kosovo, Macedonia, Montenegro, Norway, Serbia and Switzerland. The underlying data for the study is based on a combination of the ch-aviation airline knowledge base, jp airline-fleets and manual research by ch-aviation.

During the time period we observed a total of 195 regional airlines have operated in the countries under consideration, of which only 130 carriers are still active today. This means a loss of 65 regional airlines over the last five years, reflecting a significant mortality rate of 33.33%.

This rate is even more alarming when we only look at the carriers entering the market between 2008 and today: Every second newly founded carrier was unable to survive. The numbers look a bit better for the airlines that already existed before 2008. Of all 151 regionals that existed before 2008, 108 (71.52%) are still operating. They represent more than three quarters (83.08%) of today’s active carriers.

To sum things up, there has been a major airline decline over the last few years. The regional market in Europe in particular does not seem promising to start-ups. Moreover, it should be mentioned that the decline of regional airlines has a negative effect on secondary airports, frequently the bases of regionals. The cessation of a carrier can result in a drastic reduction in airport business volume, making its future uncertain.

Affiliates versus Independents: Converging Ratio

The distinct analysis of affiliated/network airlines and independent carriers revealed a current 1:2 ratio (42 affiliates/network carriers with regional operations = 32.31%, 88 independents = 67.69%; see Figure 3). This ratio has converged. In total, between 2008 and 2013, there were 49 affiliates/network carriers with regional operations (= 25.13%) and 146 independents (= 74.87%) amounting to a ratio of 1:3.

With regard to affiliates and network carriers with their own regional operations, alterations have been comparably low over the last five years. Only two new airlines were founded between then and now that fall in this category, Cimber which launched in 2012 and Olympic Air in 2008. Both weren’t new market participants in the proper sense, but rather successors: Cimber evolved from the insolvent Cimber Sterling (and works closely with SAS) and Olympic Air from Olympic Airlines.

14.29% of the affiliates withdrew from the market. In contrast, 39.73% of the independents have gone out of business. Considering only independents, the highest mortality rate could be observed between the years: A total of 42 carriers were founded from 2008 on, yet 55% of them have failed.

Fleet Development

How have fleets changed over the past five years? In 2008, 706 aircraft with 20-50 seats were operated by European regionals. Within five years, this number decreased by 53.26% to 330. There was also a decrease in the number of aircraft with less than 19 seats (by 13.79%). Only the amount of 50-100 seaters increased by 3.37% from 682 to 705 (see Figure 5). In summary, we can observe a trend away from aircraft with fewer than 50 seats towards aircraft with 50-100 seats.

It is expected that the demise of 37-50 seat regional jets in Europe will come sooner rather than later. This corresponds with a similar development in the United States where major carriers are currently slashing regional jets in this category from their contracts with regional partners very proactively, moving to higher capacity regional aircraft. Lufthansa’s regional affiliates have retired 60 50-seat aircraft in five years, as Lufthansa has decided to drop all of these aircraft and now to also drop all 70 seat turboprops by the end of 2013.

And yet, it was small regional jets like Bombardier’s CRJ-200 or Embraer’s ERJ-145 that replaced turboprops in the mid-nineties. They made flying both short and long routes with just a few passengers more economical and were considered more attractive for passengers, thereby constituting stepping stones into profitability for many regional airlines. However, triggered by the post-9/11 recession, the below 50 seat jets’ success started going south. Regional airlines that also often face competition from low-cost carriers launching the same or similar routes with a completely different business model began moving towards larger regional jets and back to turboprops (as new aircraft types with lower per seat costs have become available).

At some point, the costs of operating 50 seat jets could not be justified any longer after the fuel prices exploded coupled with the global financial crisis.[6] In order to distribute fix costs over a higher amount of seats, the majority of the carriers now focus on operating large 90-plus seat jets like the ERJ195 or CRJ-900 or slightly smaller turboprops like the ATR72-600 or Bombardier Dash 8-Q400 where routes justify the use of these aircraft. Other routes are either dropped altogether or picked up by other carriers operating smaller turboprop aircraft (that will face a problem of their own due to the lack of fleet replacement options) as no new turboprops with 20-50 seats are being offered anymore with the ATR42-600 being the only 50 seat turboprop still for sale.

Green cells = More than 20 deliveries/year of a series (e.g. Fokker70/100, EMB-190/EMB-195) Data source: ch-aviation

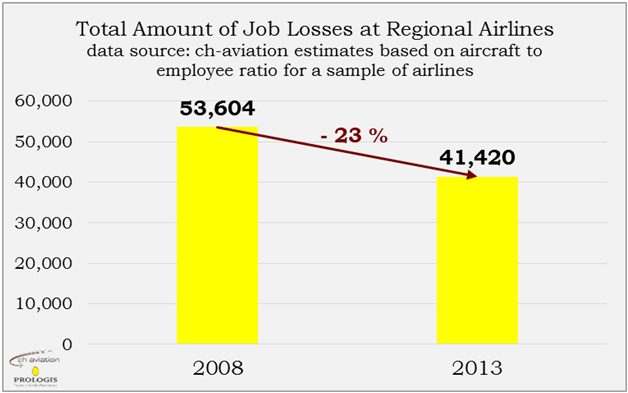

The victims: Employees

The preceding analysis results clearly illustrate the regional markets’ downturn in Europe. And, as usual, the recession’s pain is felt most by the employees.

In total, 12,184 regional airline jobs were lost in the European regions we evaluated. Based on a sample of 20 affiliated regional carriers and 20 independents, regionals in Europe currently employ a total of 36 direct and indirect employees per aircraft on average. In total, 12,184 regional airline jobs were lost in the European regions we evaluated. From a rational perspective, this means that over the last five years seven jobs were lost every day. This number probably reflects the dramatic drop in Europe’s regional aviation industry better than any previous figures referred to in this article.

When analyzing the development of jobs in Europe’s regional airline industry, we made a distinction between direct and indirect airline jobs. Direct jobs refer only to the aircrew needed to operate the aircraft, that is pilots and flight attendants. Indirect jobs include all other jobs in operations, administration and engineering. Based on PROLOGIS and ch-aviation estimates, there were 15,118 direct regional airline jobs within the EU and the other European countries we analyzed in 2008. By the beginning of 2013, this number had dropped to 11,930 (a decrease of 21%). During the same five year period, indirect jobs were reduced by 8,996 from 38,486 to 29,490, accounting for a decrease of 23%.

Conclusion and Outlook

Establishing a new airline, no matter whether it is a regional, low cost or network carrier, is a huge challenge and anything but a guarantee of financial success. However, we are still observing all of these new airline start-ups every year. This raises the question: Are the founders and investors in all of these new regional market participants aware of the high risks and low chances of success? Have they recognized the consequences that come along with a failing attempt? And, if so, what is their motivation to still keep trying to enter regional markets with new ventures? After scrutinizing Europe’s regional carriers’ development over the past five years, we believe that this industry is indeed quite challenging at its current stage. Nevertheless, there still seems to be room for growth in some regional niche markets.

When carriers are located at or fly to regions where alternatives are limited or nonexistent, there still is potential. Carriers like Direktflyg, Malmö Aviation, Nextjet and virtual operator Sverigeflyg mainly focus on the Swedish and Scandinavian regional market respectively. Widerøe primarily flies within Norway. Air Iceland offers domestic flights and routes to Greenland and the Faroe Islands. These are a few independent carrier examples with low competition from other carriers or modes of transportation which seem to work on their own or thanks to public service obligation schemes with government support in place to serve remote regions effectively. But most regions in Europe do not offer such niche conditions. And if not sheltered from competition for whatever reason (geographically, airport constraints etc.), regionals quite often have trouble keeping up with low-cost carriers from a competitive perspective, and, from a technological and organizational perspective to effectively work closely, with large international network airlines (i.e. interlining, codesharing, through check-in). So, as network carriers drop regional routes, the point to point demand on these routes is often insufficient for an existing or new regional carrier without network connectivity to take them over. Thus, it is often unlikely that these routes will be served again.

In conclusion, the current situation within Europe’s regional airline markets is no bed of roses unless independent carriers can make use of one of the few prosperous niches to settle, thrive and prosper in.

To download the following analysis as a PDF file click here.

__________________________________________________________________________________________

About Prologis and ch-aviation

ch-aviation is managed by a team of passionate aviation professionals from Switzerland, Germany and Austria. Since 1998 www.ch-aviation.ch offers a wide range of tools and search options targeted at aviation industry professionals to get access to:

the most extensive and up to date airline knowledge base in the world. It provides comprehensive weekly news updates covering global airline industry developments with a focus on:

– strategic network and fleet developments,

– airline start-ups and bankruptcies as well as mergers, acquisitions and strategic partnerships.

– Weekly Airline Route Network Update systematically track network changes of over 700 airlines worldwide.

ch-aviation also tracks more than 37.500 individual aircraft, in excess of 5.500 airports and airlines with access to worldwide airline schedules and route networks.

PROLOGIS ranks as one of the world’s leading management consultancies that specialize in the aviation industry thanks to its more than 15 years of experience and over 45 airline customers served.

With an average of 7 years of practical experience working for airlines, airports and ground handling companies, the PROLOGIS consultants are recognized experts on the following topics:

– Distribution & Revenue Management

– Ground Operations & Airport Processes

– Revenue Accounting

– Network Planning & Scheduling

– IT Services (System Migration, Evaluation and Implementation)

– Financial Controlling and Data Warehousing

Thanks to the many international projects on behalf of network, regional, low-cost and charter airlines from more than 30 different countries, PROLOGIS offers best practices and integrate these into their customers’ existing structures and cultures. Whether it’s strategies, processes or systems, the PROLOGIS team works together closely with the customers to find the best possible solutions for the challenges at hand.

__________________________________________________________________________________________

Copyright @ 2013 PROLOGIS AG & ch-aviation GmbH

All rights reserved. This study or any portion thereof may not be reproduced or used in any manner whatsoever without the express written permission of the publisher except for the use of brief quotations embodied in critical reviews and certain other noncommercial uses permitted by copyright law.